Durable and diverse drivers for small caps

June 2026

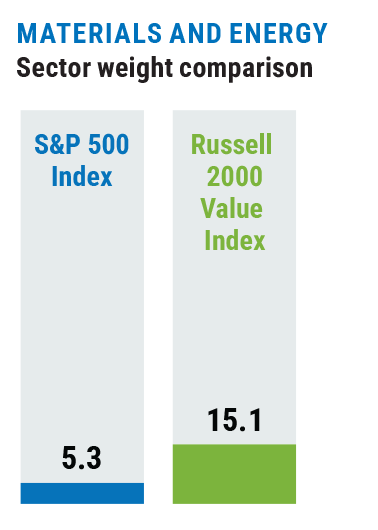

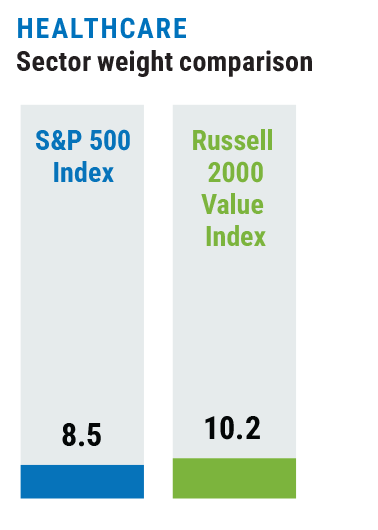

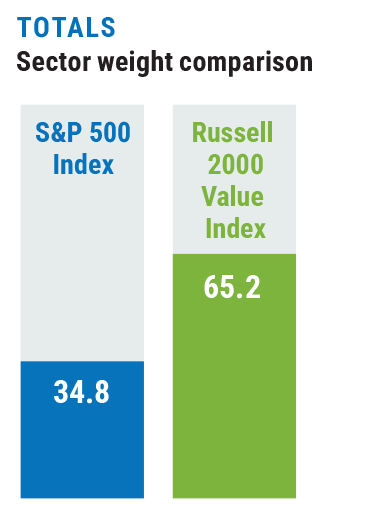

We believe the environment for small-cap cyclicals is as attractive as it has been in more than two decades. Returns on capital are improving as manufacturing recovers, energy costs remain supportive, and a once-in-a-generation infrastructure buildout continues to gain momentum. What makes this cycle especially compelling is its breadth: We see tailwinds across industrials, building products, energy services, financials, and manufacturers all at the same time. And as large-cap index concentration continues to rise, the diversification case is hard to ignore—industrials, materials, financials, and energy make up just 28% of the S&P 500, but those four sectors are more than 50% of the small-cap value index. In other words, the small-cap market remains one of the few places to find meaningfully diverse sector exposure.

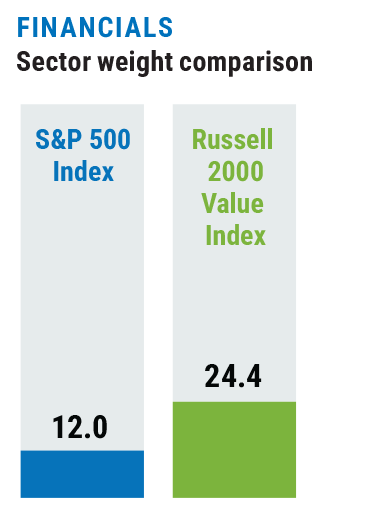

Financials: Structurally higher rates are a tailwind

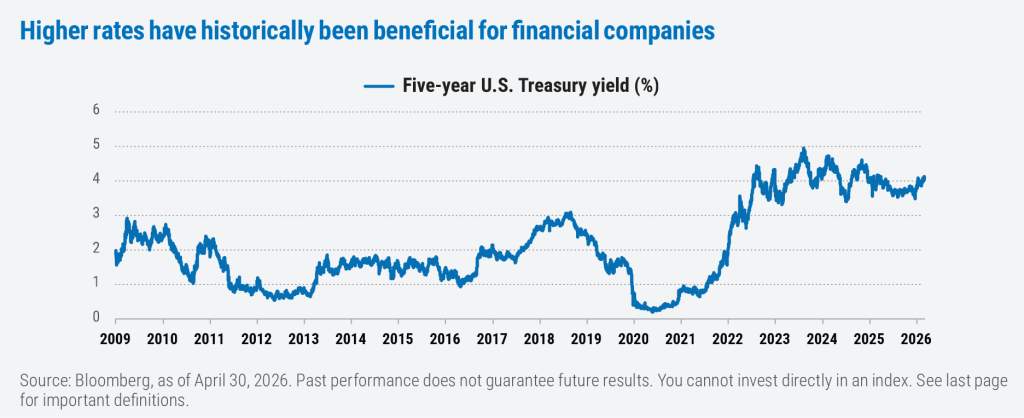

Higher rates are generally a tailwind for the Financials sector, which represents nearly a quarter of the small-cap value universe. After more than a decade at unusually low levels, short- and long-term rates appear likely to remain higher for longer—there’s no evidence to suggest a return to a zero-rate policy backdrop anytime soon. That matters because the easy-money era favored a style of investing that rewarded distant cash fl ows and story-driven growth. In our view, it also held back the kinds of businesses we focus on: profitable, cash-generative small caps that often trade at single-digit earnings multiples.

When real interest rates are positive, capital has a clearer price tag. Companies that cannot fund operations with internally generated cash flow face a higher bar to raise money. That dynamic is usually a headwind for unprofitable growth companies and a tailwind for the types of free-cash-flow-generative small caps that make up the core of our portfolios. Higher rates can also benefit small-cap financials specifically through higher net interest margins. Over time, we expect the market will revert to the mean and reward solid earnings and positive cash flow more consistently than it does speculative narratives—and higher rates are a catalyst for that shift.

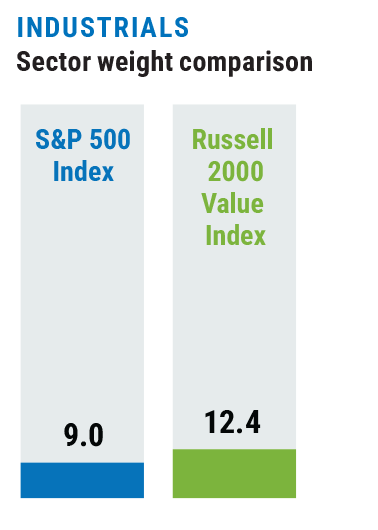

Industrials: Manufacturing PMIs appear to be at an inflection point

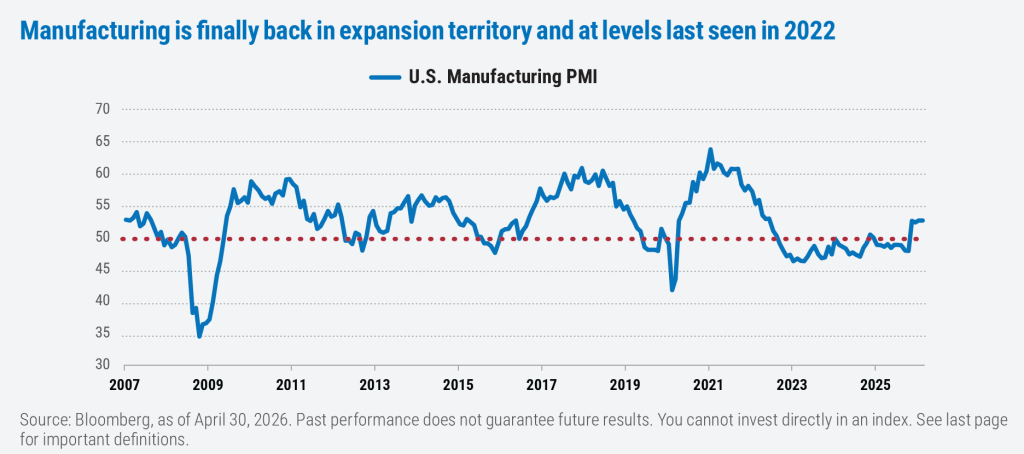

The U.S. Manufacturing PMI has turned higher after more than three years below 50, a level that signals contraction. For small-cap investors, this is one of the most important indicators to watch. Small-cap companies tend to be more domestic focused, more sensitive to changes in volumes, and more tied to the real economy. When manufacturing slows, earnings often fall quickly; when it rebounds, operating leverage can drive a sharp recovery.

Historically, the shift from PMI contraction to expansion (marked by readings above 50) has been a strong catalyst for small caps. The reason is simple: Large-cap multinationals can often offset domestic weakness with overseas exposure, while small caps usually cannot. When the cycle turns, small companies tend to feel it first—and benefit more directly. We believe this inflection supports a durable earnings recovery across industrials, building products, auto parts suppliers, and consumer-facing manufacturers where inventories have normalized.

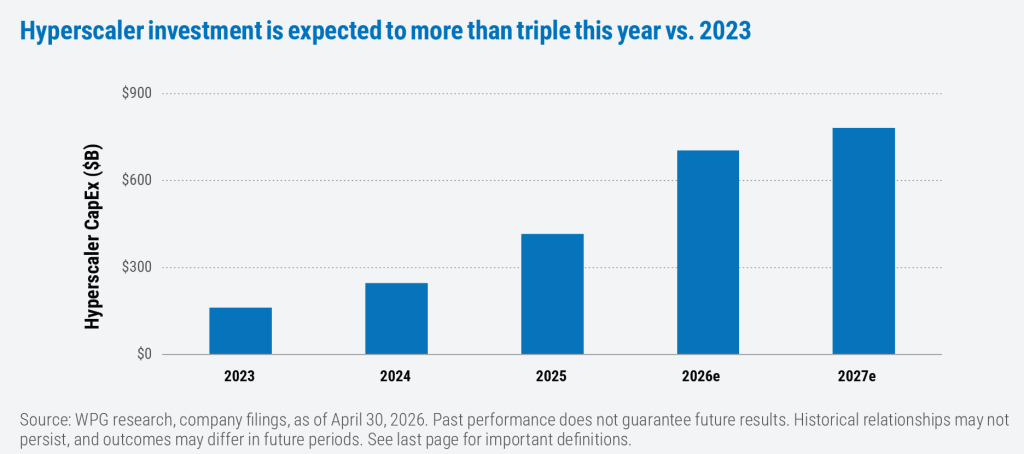

When investors think of the Tech sector these days, they probably think of high-flying chip makers and the Magnificent 7. The AI spending spree among the latter companies shows no signs of slowing: Capital expenditures (CapEx) from the major hyperscalers (Microsoft, Amazon, Google, and Meta) has already more than doubled—from roughly $150 billion in 2023 to over $400 billion in 2025. Many industry estimates point to further growth, potentially reaching $700–800 billion by 2027.

But building data centers takes far more than chips. It requires steel and copper, switchgear, HVAC systems, backup generators, modular construction, and extensive electrical infrastructure. It also drives investment in power generation and transmission—benefiting not only utilities, but also engineering firms and equipment suppliers, many of which are Industrials companies still trading at attractive valuations. We view the AI infrastructure buildout as a multi-year demand driver for small-cap industrials, and we believe it is still early in the build-out process.

Materials and Energy: The United States is now in an advantageous

cost position

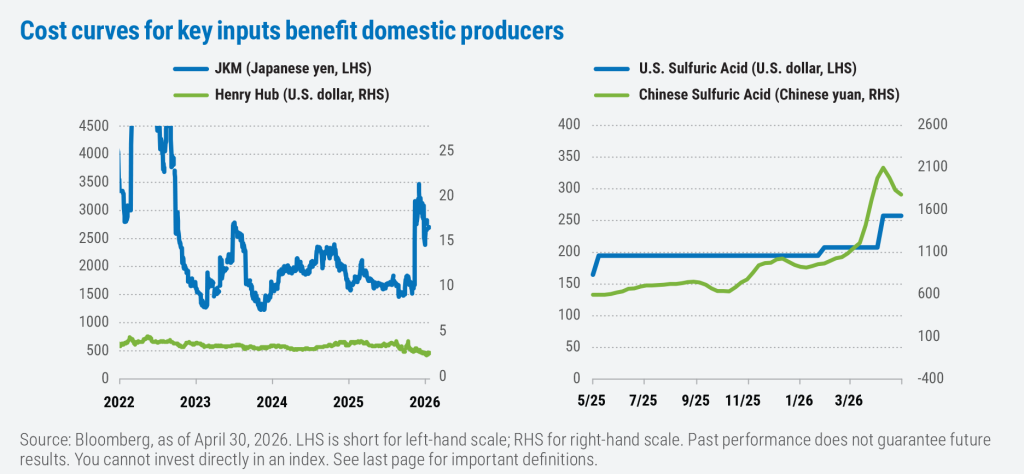

The gap between Asian liquefied natural gas (LNG) prices (often referenced by the Japan Korea Marker, or JKM) and U.S. natural gas prices (Henry Hub) has widened through early 2026. Henry Hub prices have stayed relatively steady in the low single digits, while JKM has moved sharply higher in yen terms, reflecting tight global LNG supply and strong demand in Asia.

This matters for small-cap equities in a few ways. First, it supports U.S. LNG-related businesses such as midstream operators, compressor manufacturers, and oilfield service firms. Second, lower and more stable domestic energy costs give U.S. manufacturers an advantage versus many European and Asian competitors, where energy remains meaningfully more expensive. For the companies we own, that cost backdrop can help protect margins as volumes begin to recover.

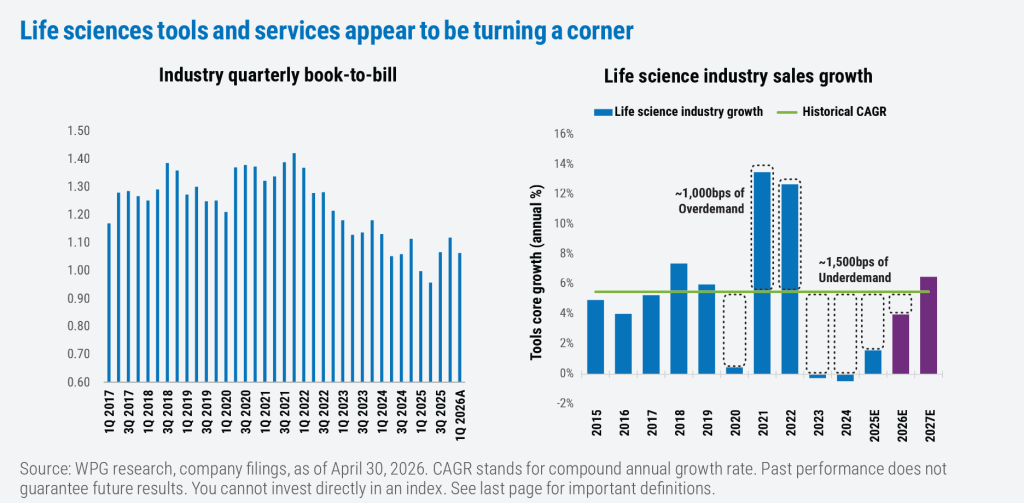

Healthcare: Green shoots in tools and diagnostics

In the wake of the COVID-19 pandemic, biotech funding and accelerated clinical timelines pushed book-to-bill ratios above 1.35x in 2021. (Book-to-bill ratios compare orders received with orders fulfilled, and ratios above 1.0 generally indicate strong demand.) The subsequent funding slowdown pulled the ratio below 1.0x through much of 2024 and 2025—meaning companies worked through backlog faster than new orders arrived. That dynamic now appears to be turning: Recent quarterly data shows book-to-bill back above 1.0x, consistent with a bottoming in new awards.

The broader life science tools industry tells a similar story. Annual sales growth surged above its long-run pace of roughly 5.5% yearly growth during the pandemic demand spike, then fell well below trend during the correction. Current estimates for 2026 and 2027 point to a return toward trend-line growth, suggesting the destocking and budget-tightening cycles that weighed on many small-cap tools and diagnostics names are largely behind us. For a part of the market that has been overlooked as investors focused on large-cap pharma and GLP-1 narratives, the setup is becoming more interesting.

Conclusion

Important disclosures

The views expressed in this commentary refl ect those of the author as of the date of this commentary. Any such views are subject to change at any time based on market and other conditions and Boston Partners disclaims any responsibility to update such views. Past performance is not an indication of future results.

Discussions of securities, market returns, and trends are not intended to be a forecast of future events or returns. You should not assume that investments in the securities identified and discussed were or will be profitable.

Risk considerations

The views expressed reflect current market observations and are subject to change. Investments in small-cap equities involve risks, including greater volatility, lower liquidity, and increased sensitivity to economic conditions relative to larger companies. The trends and tailwinds described may not persist, and there can be no assurance that the anticipated benefits of improving fundamentals, higher interest rates, or sector-specific developments will be realized. Changes in interest rates, inflation, or economic growth could adversely affect the sectors discussed, and companies may not experience the expected operating or earnings improvements. Investors should consider these risks alongside the potential opportunities described.

Terms and definitions

Hyperscalers are large-scale data centers used for cloud computing and data management, and can refer to the companies that provide such services. The Magnificent Seven stocks are a group of high-performing and influential companies in the U.S. stock market: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Institute for Supply Management’s (ISM) U.S. Manufacturing PMI is a key economic indicator that measures the activity level of purchasing managers in the manufacturing sector.

The Russell 2000 Value Index tracks the performance of those small-cap U.S. equities in the Russell 2000 Index with value style characteristics. The S&P 500 Index tracks the performance of the 500 largest companies traded in the United States. It is not possible to invest directly in an index.

Boston Partners Global Investors, Inc. (Boston Partners) is composed of three divisions, Boston Partners, Boston Partners Private Wealth, and Weiss, Peck & Greer (WPG) Partners, and is an indirect, wholly owned subsidiary of ORIX Corporation of Japan (ORIX).

8970113.1

Eric Gandhi, CFA

Portfolio Manager

Emil Friis

Research Analyst

WPG Select Small Cap Value

A concentrated portfolio of our highest-conviction small-cap ideas managed by the veteran team at WPG Partners.

WPG Partners Small Cap Value Diversified

A more broadly-diversified portfolio of small-cap stocks built on WPG’s time-tested approach.